“My wallpaper and I are fighting a duel to the death. One or the other of us has got to go.”

– Oscar Wilde’s last words (maybe)

It may have gone without much mention, but late last year the British Library reinstated Oscar Wilde’s library card, which had been, with curt promptness, rescinded in 1895 due to his incarceration for “gross indecency.”

Source: The British Library

It’s a nice thing to have done, I guess, to have restored the privileges of a man who has been dead for 125 years— though the British Library did stress that this gesture was symbolic, which seems a bit tautological. Oscar Wilde is not walking through the door demanding to check out a copy of Piranesi. And if he did, well, I’d be damned if that’s not the coolest thing to have happened at the British Library in quite some time.

(The British Library doubled down on the symbolic nature of his reinstatement by making the expiration date for the card November 30, 1900. Can’t be too careful, I guess.)

Even before the reissuing of his library card, several of Oscar Wilde’s original works had been housed at the British Library, including handwritten versions of The Importance of Being Earnest and, in what must be described as a gross irony, De Profundis, which he wrote to Lord Alfred Douglas, who was his lover.

In late 19th-century England, being gay was a crime: a “gross indecency.” As Oscar Wilde wrote in De Profundis, “Society…will have no place for me,” and yet he closed with a notion of pure beauty, claiming that nature would “hang the night with stars so that I may walk abroad in the darkness without stumbling, and send the wind over my footprints so that none may track me to my hurt: she will cleanse me in great waters, and with bitter herbs make me whole.”

Is Berkshire Hathaway better off without Warren Buffett?

Times change. Oscar Wilde – for better or worse – was a creation of his time and environment. His enduring value as an author and his rejection by his society are two sides of the same coin. Though his example is extreme, it is true of all of us. In The Psychology of Money, Morgan Housel writes of the “one-in-a-million” lucky break that Bill Gates attended one of the few schools in the world that had access to a computer in 1968.

I was thinking of Wilde and Gates as I watched the replay of this year’s Berkshire Hathaway annual meeting, the first without investor extraordinaire Warren Buffett as chairman. Buffett’s success as an investor is without question. But Warren Buffett’s skill as a manager of a conglomerate comprising more than 60 businesses is also formidable. But just as Buffett was a product of his timing as an investor, I have to wonder if, in a world of rapid change driven by artificial intelligence, new CEO Greg Abel isn’t better suited than Buffett would be to run Berkshire Hathaway.

Due to a personal conflict, I was unable to attend this year’s Berkshire meeting. But in the last few, I’ve been struck by the amount of time given to discussion of how GEICO*, a Berkshire-owned subsidiary, has fallen behind its competitors. Other components of Berkshire Hathaway’s empire, including BNSF, Dairy Queen, and Fruit of the Loom, have, to varying degrees, failed to achieve their best selves. Warren Buffett’s big decisions have centered around what to buy. Greg Abel, on the other hand, grew into his current role by being an operator, most notably in the highly regulated utility space. Buffett has warned for years that Berkshire’s ability to make meaningful transactions was likely limited. Is the company’s future going to be driven instead by Abel’s ability to improve the performance of the companies that Berkshire already owns?

The AI-generation CEO

Matthew Prince wrote an article recently in which he discussed how the company he leads, Cloudflare, laid off more than 20% of its workforce. This, despite the fact that, objectively, Cloudflare continues to grow quickly.

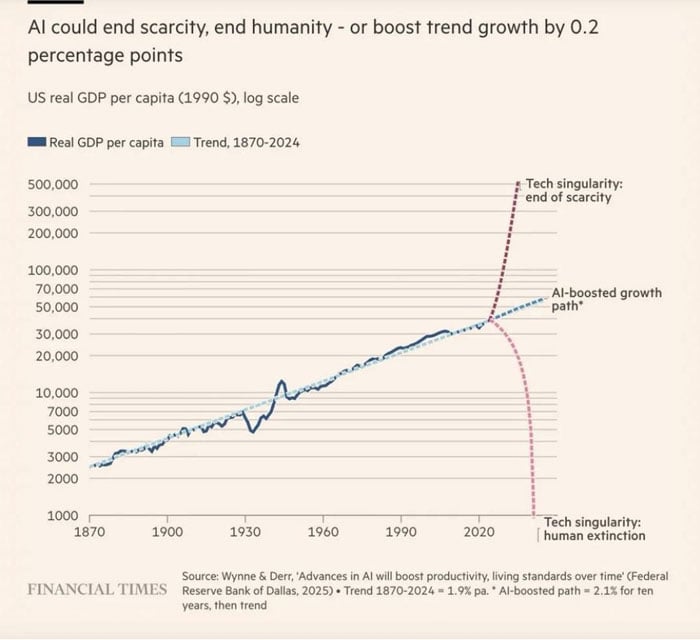

There is a huge amount of confusion, consternation, and even fear around how AI will impact, well, everything. This was perhaps most well articulated by what might be the funniest graphic ever run in the Financial Times1:

Anecdotally, I hear from employees across companies who are being tracked not based upon their output from AI, but simply their usage of it. Burn a lot of tokens, no questions will be asked. Just a few days ago, Uber’s COO questioned the return on their investment into AI, as it burned through its entire annual AI coding budget by the end of April.2 Other companies that are openly questioning their return on investment include Microsoft and Duolingo.

The question of culture and return on investment from AI will be a massive determinant of winners and losers in this space in the next decade. Matthew Prince noted that where AI is making the biggest change is in their need for “measurers,” or what the anonymous author Educated Guesser calls “context carriers.”

The theory isn’t new. Peter Drucker noted in “The Practice of Management” back in 1955 that the two basic functions of any business are marketing and innovation. Everything else within the business is a cost. Not that there aren’t fantastically talented and necessary people within these components, just that AI can measure crucial components within a company with a ruthless objective efficiency with which people cannot compete.

The ability to manage in an AI-native way requires a skillset that many of the best leaders from even a decade ago would have lacked. Those leaders landed in the stream at the right time. And it goes without saying that Prince might not be right about this as well. What is a good sales trainer worth, even though that role is, in Drucker's math, a cost? What value do a middle manager’s underwriting ideas have? Or a human measurer making contextual leaps?

Almost nothing is clear, except that if Peter Drucker was right, the path to success in an AI world will be to become instrumental in the act of innovating products or selling them. Roles that involve measuring or contextualizing are likely to become fewer and further between, though the people who succeed at them are likely to be extremely valuable to their organizations. At the end of the day, The Financial Times chart may be right: AI could boost trend growth by a few basis points, but what an AI-driven economy looks like is still extremely cloudy.

Related Posts

Sell in May and Go Away? Here’s Why Investors Shouldn’t Take the Summer Off.

Back in 1986, The Stock Trader’s Almanac coined the phrase “sell in May and go away” to highlight...

There are 4,740 ETFs out there. How can you choose where to put your investment dollars?

Ever tried to figure out what to order for dinner on a Friday night? Perhaps you can relate to the...

The Same Stream Twice

Mann on the Street

“My wallpaper and I are fighting a duel to the death. One or the other of us has got to go.”

–...