Are you ready to take the bull by the horns, so to speak!

You've been putting money aside and are now set to start investing.

Now comes the decision: Where should you put your money? In a passive fund—like an index mutual fund? Or perhaps in an active exchange-traded fund (ETF)?

Well, if you've seen the data showing that passive managers have done better during the prolonged bull run that began after the 2008 Global Financial Crisis, then the answer seems cut and dry.

But before you make the decision, we think there is one important question you should ask:

- Why does passive management seem to have better returns than active?

The answer to this may surprise you and cause you to rethink your choices.

Why has passive appeared to outperform active?

Passive investing, which tracks a specific index, is designed to match, but not beat, the market performance. On the other hand, active investing has the potential to outperform the market. But herein lies the issue with the data that show passive outperforming active: Not all active management is genuinely active.

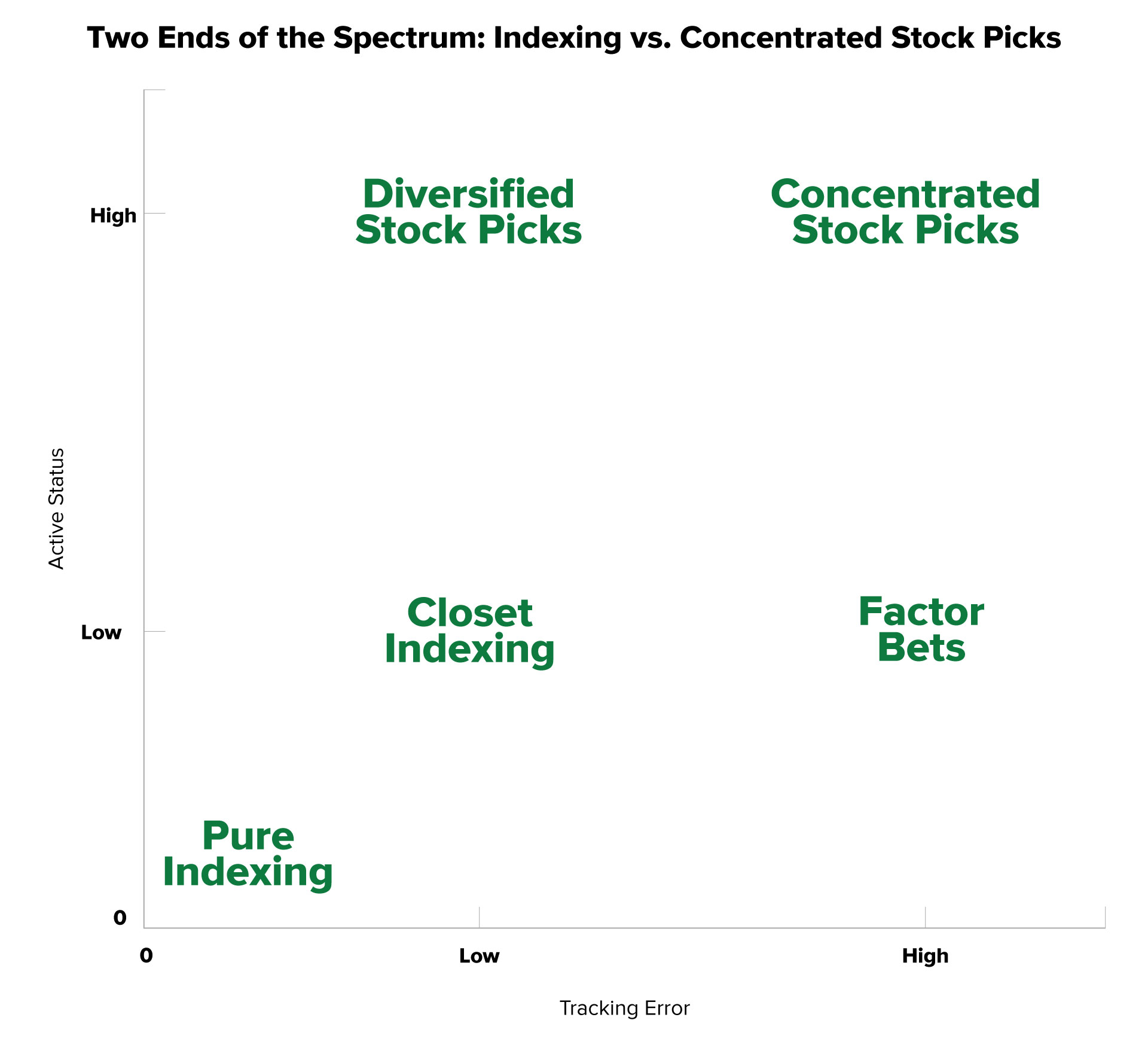

Source: How Active is Your Fund Manager? A New Measure That Predicts Performance, Mar. 21, 2006, Updated Feb. 9, 2019

This chart shows that some managers are "closet indexers," meaning they track closely to the index and don't take positions that differ (even though clients are paying active management fees). Concentrated portfolios with high active share and high tracking error are at the other end of the spectrum.

What is active share?

The measure of active share was developed in 2006 by Yale professors Martijn Cremers and Antti Petajisto to define active management. It assesses how much a manager actively manages a fund by measuring the percentage of investment holdings in a portfolio that differ from the benchmark index. (Tracking error is similar, but instead of measuring holdings variance, it looks at the volatility of a portfolio’s return relative to a benchmark’s return.)

Active management has an active share of 60% or higher. In contrast, an active share of 20% to 60% indicates closet indexing, and less than 20% is passive management.1 So when the data show passive outperforming active, you should ask: Are the active funds defined by active share? Not likely.

The concept of active share can be hard to grasp, but think of it like this:

You need a new pair of pants. All your friends purchased the same blue pants, so you’re considering buying them too. But after trying them on, you feel they lack some characteristics that make up a quality pair of pants. So instead, you try on a different pair. These pants fit you well—the length is just long enough, the material is soft and comfortable, and the waist, hips, and inseam are almost tailor-made for you. What do you do? Of course, you buy several pairs in various colors. While you still have other pants in your closet, these new pairs make up a high percentage of your pants wardrobe. Should you care whether your friends buy these pants too? Probably not.

That's what active share is. A portfolio manager finds a company that she believes has customer loyalty, increasing market share in a growing industry, and is led by a knowledgeable and consistent management team. She has high conviction in this stock, so she buys a sizable portion for an ETF she manages. Should she care if this stock isn't in an index or if the fund owns a lot more of it? No, she shouldn't. Because a shareholder of that active fund is paying for that portfolio manager to find perceived gems and put a stake in the ground. Not a twig, but a steel rod stake!

Now to perhaps the most crucial question: Does active share have any bearing on performance?

It does, according to Cremers and Petajisto's research. They found that high active share portfolios outperformed by 1.13% to 1.15% per year over 10 years (1992–2003).2 Importantly, this outperformance is after fees and transaction costs. In contrast, funds with the lowest active share underperformed by 1.42% to 1.83% per year over that same period.2

And another timely question: How does high active share hold up during a recession? Petajisto updated the study in 2010 to capture the significant market decline in 2008. He found that from 2008 to 2009, the results were consistent with historical findings. During those two years, funds with high active share outperformed their benchmark by almost 1% annualized net of fees, while all other funds underperformed their respective indices.3 Now, this study only looked at a short time frame to assess the performance during only one recession—the 2008 Global Financial Crisis. So while we can look at the findings as one data point, we cannot determine a trend or say that future performance will reflect this particular historical result.

Ok, let’s summarize what we’ve learned.

- First, not all claims of active management are truly active. The most “active” are concentrated stock portfolios that exhibit both active share greater than 60% and high tracking error to a benchmark. Yet, the fees charged by active managers—regardless of if they are indeed "active”—may not be all that different.

- Second, a high active share of greater than 60% has the potential to produce better long-term results than lower active share portfolios.

- Finally, the key is long-term performance.

Long term is key

High active share, especially in concentrated funds, could also mean that these funds could underperform in the short term, possibly significantly. That’s because a high active share fund, particularly one with security concentration, may get hit with idiosyncratic risks—risks specifically arising from an individual company.

In the short term, a company's performance can vary due to its business, new investments, growth objectives that may take time to play out, and other factors. Therefore, returns of a concentrated fund can be significantly affected when the market turns away from these stocks. We expect this in the short term from time to time.

But over the long term, high-conviction, high-active share funds could outperform. Subsequent research on active share shows that among high active share funds, only those with long holdings—rather than those with rapid turnover—outperform on average.4 "In other words, only active stock pickers with strong, long-term convictions are successful. To quantify this finding, the study found that in portfolios where both Active Share and holding durations are in the top quartile, alpha (return above the benchmark) is 1.94% a year. By contrast, in portfolios where Active Share is in the top quartile but holding duration is in the bottom quartile, alpha is –1.15% a year."4

High active share alone is not enough

Not everyone believes in active share. Some studies even refute the significance that these studies show. Some investors believe that active share is not as useful as a stand-alone measure but may be useful in conjunction with other variables.

So, we look at high active share in two ways: First, as an indication of actual active management, and second, as a representation of a high level of conviction. If managers have a firm belief, they would be less concerned with how their fund matches up to the benchmark. In contrast, managers with less conviction may introduce benchmark holdings to compensate for uncertainty, leading to a more index-like portfolio.

But high active share by itself can’t guarantee future performance. Neither can only looking at a fund's past performance. Instead, we believe, high active share in conjunction with other factors such as market opportunity (finding strong companies at undervalued prices) or superior security selection (picking the right stocks) is more likely to lead to outperformance over the long term.

Related Posts

Sell in May and Go Away? Here’s Why Investors Shouldn’t Take the Summer Off.

Back in 1986, The Stock Trader’s Almanac coined the phrase “sell in May and go away” to highlight...

There are 4,740 ETFs out there. How can you choose where to put your investment dollars?

Ever tried to figure out what to order for dinner on a Friday night? Perhaps you can relate to the...

The Same Stream Twice

Mann on the Street

“My wallpaper and I are fighting a duel to the death. One or the other of us has got to go.”

–...